Iran War is Jolting (and Could Break) the Region's Economic Order

The costs are mounting across sectors and countries. Is this a temporary shock or the start of a deeper repricing of risk in the region?

Open conflict involving Iran is already generating real economic costs: damage to physical infrastructure across the region (e.g. airports, hotels, AI data centers, energy infrastructure), insurance premiums are skyrocketing, a near total blockage of the Strait of Hormuz, and a spike in oil prices. But it is too early to know whether this is a temporary shock or something longer-term. With its fair share of conflicts big and small, the Middle East never fails to surprise. Although many permutations are possible, we see several scenarios emerging, each with historical precedents and similarities:

Scenario 1: Sharp shock, rapid recovery: A relatively short conflict (measured in weeks) stabilizes through quiet diplomacy and tacit de-escalation by the major powers. Energy flows resume, shipping lanes reopen, and the initial spike in insurance premiums and commodity prices gradually recedes as markets regain confidence that escalation is contained. The conflict ultimately looks like a severe, but temporary shock layered onto the region’s longstanding geopolitical risk premium. The Gulf’s economic transformation narrative, and push to become a global hub for capital, trade, and tourism, remains intact. As with the 12-day war in June 2025, investors shrug their shoulders and treat the conflict as yet another sporadic outbreak of regional volatility rather than a reason to exit the market altogether.

Scenario 2: Protracted conflict, structural economic impacts: A longer war (months or longer) between the remnants of the regime and a coalition of U.S., Israeli, and possibly some regional forces generates sustained disruptions to energy infrastructure, shipping lanes, and regional commerce. The Strait of Hormuz remains under intermittent threat, including from the Houthis, forcing global energy markets to adapt to new supply routes while shipping and insurance costs remain elevated. Iran leans heavily on asymmetric retaliation, turning the conflict into a drawn-out war of attrition on multiple fronts, including beyond the Middle East. Over time, markets start pricing a higher risk premium for the broader region, making capital more expensive and slowing the Gulf’s ambitions to position itself as a safe, stable hub for investment.

Scenario 3: Internal fragmentation and regional proxy competition: The conflict weakens Iran internally, opening the door to competing factions, insurgent movements, and regional actors backing different groups inside the country. As in Iraq post-2003 or Syria post-2011, external actors begin backing rival political and military actors, turning Iran into a fragmented conflict zone rather than a unified actor. The resulting instability prolongs violence, complicates energy and export activity, and creates new security risks along Iran’s land borders (which exceed 3,600 miles in length and are shared with Iraq, Türkiye, Azerbaijan, Turkmenistan, Afghanistan, and Pakistan). In this scenario, economic impacts come less from a decisive shock and more from chronic instability that could hamper trade flows, global energy markets, and regional alliances.

The Middle East has always found a way to absorb volatility, but the magnitude and stakes of this conflict are greater. The difference will come down to the war’s duration and spread, whether trade routes remain open, and whether investors begin to question the region’s core economics. The situation is dynamic, and moving faster than either of us can refresh our feeds. Having said that, here are a handful of the key themes we are closely monitoring:

Energy Markets Under Strain

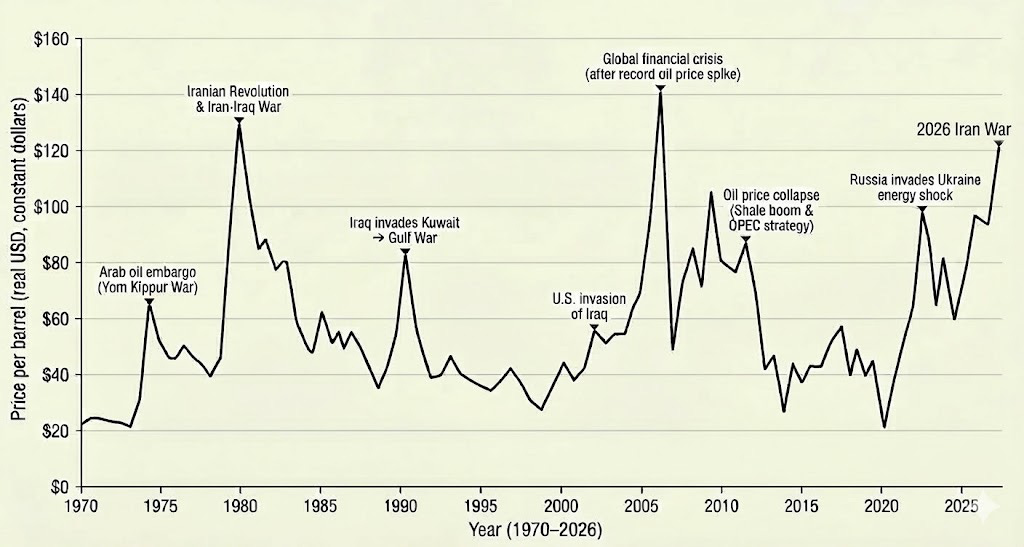

The energy market is the most immediate domain in which the Iran conflict is affecting the global economy, although the scale of the shock will depend heavily on duration. The central issue is the Strait of Hormuz, which normally carries roughly a quarter of global seaborne oil trade and about a fifth of LNG shipments. Tanker traffic through the chokepoint has slowed to a near standstill amid missile and drone threats, rattling traders who only weeks ago expected a global crude surplus.

The conflict is touching physical energy infrastructure across the Gulf: QatarEnergy temporarily halted operations at Ras Laffan, the world’s largest LNG export facility, Saudi Arabia suspended operations near the Ras Tanura refinery and terminal after drone strikes (although it announced it would restart the refinery just this week), and Israel has shut some offshore gas fields, forcing Egypt to seek alternative LNG imports.

Interestingly, East Asian governments are already moving defensively. China has reportedly told refiners to suspend diesel and gasoline exports, and Japanese refiners are urging the government to tap strategic reserves, highlighting how quickly the shock is cascading outside the region. In a further sign of how governments are scrambling to stabilize supply, the U.S. Treasury Department’s Office of Foreign Assets Control recently issued a temporary 30-day sanctions waiver allowing Indian refiners to purchase Russian crude already at sea, a stopgap measure intended to keep oil flowing into global markets amid the disruption. And the International Energy Agency, a coordinating body for 32 countries that collectively maintain strategic petroleum reserves, has said it would release 400 million barrels of oil in the market, 172 million of which are to be released by the US. This would be the largest coordinated release since the organization’s founding in response to the 1973 Arab embargo.

Brent Crude Oil Prices (1970–2026, adjusted for inflation)

Source: U.S. Energy Information Administration

Early stabilization signals would include a resumption of tanker insurance coverage and traffic through the Strait of Hormuz, Qatar restarting LNG exports at scale, and Gulf producers shifting barrels through pipeline bypass routes in Saudi Arabia and the UAE.

If those indicators materialize relatively quickly, the market could treat the episode as yet another geopolitical premium layered onto oil prices rather than the beginning of a sustained supply shock. Oil prices returned to the mid-$80s after nearly hitting $120 earlier this week, reviving fears about the type of energy-driven inflation shock last seen after Russia’s full-scale invasion of Ukraine. The situation remains volatile; as of this writing, oil prices surged back toward $100 a barrel after two tankers were attacked in Iraqi waters. These attacks offer a stark reminder that energy infrastructure across the entire region is at risk, not just in the Strait of Hormuz, and that even the IEA’s historic reserve release may be insufficient to offset ongoing disruptions.

Chokepoints and Commerce: Trade, Shipping, and Logistics

The conflict is also spilling into the Gulf’s trade, travel, and logistics corridors, demonstrating how indispensable the region is to global commerce. Tanker traffic is reportedly down 90% from a week and a half ago. Iran has reportedly deployed dozens of mines in the Strait of Hormuz — retaining the capacity to deploy hundreds more — prompting the U.S. military to destroy 16 Iranian minelaying vessels, although even partially mined waters could extend shipping disruptions well beyond any ceasefire, as clearance operations typically take weeks or months.

Ports in the UAE, Oman, Bahrain, and Saudi Arabia are central nodes in transcontinental shipping between Africa, Europe, and Asia. In recent days, several of these ports have been hit by Iranian drone strikes and major global container shipping companies have canceled bookings and diverted all ships away from the region and around the Cape of Good Hope instead. We saw this bypass in late 2023 when the Houthis began a campaign of sustained attacks on commercial vessels traveling through the narrow passage in the Red Sea, which leads to the Suez Canal, a major transcontinental trade artery. Cape of Good Hope routes can add up to two weeks of transit time and higher operating costs. The current conflict has now extended that volatility to the Strait of Hormuz, pinching both of the region’s core maritime routes.

For companies still sailing in the Gulf, maritime insurance premiums are also skyrocketing, adding hundreds of dollars to the cost per container on a typical large container ship, as war-risk coverage for a single voyage can climb into the millions of dollars compared with only tens of thousands in normal shipping lanes. In an attempt to keep these shipping lanes open, President Trump announced that the U.S. Navy might escort commercial ships through the Strait of Hormuz and the U.S. Government announced that it will backstop insurance policies for companies moving goods and energy through the strait.

Airports across the region—and the skies above—have been similarly impacted. Airports in Kuwait and Dubai have both been hit. Dubai International Airport, the world’s busiest airport for international passenger travel and one of the largest air-freight hubs globally, briefly closed, but has begun gradually resuming operations this week. In a concrete sign of how the conflict is upending travel and logistics from major carriers, British Airways announced it would cancel all flights to Amman, Bahrain, Doha, Dubai, and Tel Aviv until later this month, and to Abu Dhabi until later this year. Meanwhile, the cost of sending goods from Asia to Europe has risen by nearly 50% since the war begun, according to some estimates.

Whether the conflict is short or lingers, it is already clear that the disruptions to global commerce are extending well beyond the energy supplies the Middle East has long provided. They underscore how deeply integrated the region has become in global trade and logistics.

Regional [Re] Alignment?

One of the more consequential risks of the Iran conflict is whether it forces a strategic realignment across the Gulf. In the months before the current escalation, most Gulf governments actively sought to avoid this scenario, instead lobbying Washington earlier this year to avoid a direct confrontation with Iran. Several powers, notably Saudi Arabia and the UAE, spent the years prior to the 10/7 Hamas attacks on Israel cautiously rebuilding relations with Iran to reduce regional tensions. This war, however, is pulling them back into a contest they had hoped to sidestep. Commentary from figures such as former Saudi intelligence chief Prince Turki al-Faisal and Kuwaiti academic Bader al-Saif reflect frustration that Gulf states are becoming principal actors in a conflict they did not choose.

A key question for markets and policymakers is whether these states remain defensive or begin aligning more overtly with the US-Israel camp. Early signals are ambiguous. A recent phone call between Saudi Crown Prince Mohammed bin Salman (MbS) and UAE President Mohammed bin Zayed (MbZ)—two leaders whose countries experienced elevated tensions recently over differing approaches to important regional conflicts, notably Yemen and Sudan—suggests a renewed effort to coordinate security policy as regional tensions rise.

Some have hinted that a direct Iranian strike on Gulf infrastructure could trigger a far more forceful response than in past crises. For example, influential Saudi commentator ‘Ali Shihabi suggested that a major Iranian attack comparable to the 2019 strike on Saudi oil facilities could lead Riyadh to target Iran’s Kharg Island export terminal, through which the majority of Iran’s oil exports pass. The UAE, which has generally pursued a cautious posture toward Tehran, is also an important player to watch. MbZ’s recent Tweet emphasizing national readiness and unity, as well as comments stating that the UAE “...has thick skin and bitter flesh; we are not an easy prey,” underscore that Gulf governments are preparing their populations for a period of heightened risk. If these states move from hedging between Iran and Western partners toward deeper security coordination with Washington and each other, the geopolitical map of the Gulf, carefully recalibrated over the past several years, could shift again in ways that outlast the conflict itself.

Capital Under Fire

The Gulf has worked hard to transform itself from a source of capital (courtesy of its abundant energy resources) to a destination for that capital, an idea that has gained traction recently. Traveling through the Middle East just last month, President and Chief Operating Officer of Blackstone Jon Gray said he saw a “tipping point” for deals in the region. There has been a visible bump in activity and focus from global banks, private equity firms, and investors committing large sums of capital in the Gulf’s booming infrastructure, technology, and tourism sectors.

Vision 2030 has focused on transforming Saudi Arabia’s economy and society from within. In order to be so inwardly focused, the Kingdom’s foreign policy has been predicated on preserving order and keeping conflict away from its doorstep. From reaching an informal truce with the Houthis in Yemen (although a formal peace deal has yet to materialize) to co-leading diplomatic efforts alongside the US to manage the conflict in Sudan, the Kingdom has pursued regional calm across the board.

Meanwhile, the UAE’s brand has been that of a prosperous island of stability: a five-star, high-tech, modern, Arab version of Singapore or New York. Abu Dhabi and Dubai consistently top the rankings for the world’s cleanest and safest cities, and the Emirates has become a veritable melting pot of expatriates and a global commercial hub. Drones and missiles have begun disrupting daily life in the UAE, but the government has moved quickly to reassure its population and project confidence. The tourism sector is also absorbing significant damage. The conflict is costing the region’s tourism industry an estimated $600 million per day in lost visitor spending, according to the World Travel & Tourism Council, with over 80,000 short-term rental bookings in Dubai alone cancelled in a single week and roughly 4 million travelers stranded by five days of regional flight cancellations. Even as Iranian drones struck, the UAE announced the completion of a comprehensive economic agreement with Japan, an act of both defiance and forward-looking intent.

According to some calculations, the UAE has spent upwards of $1 billion per day to defend itself against Iranian attacks. The economic consequences of sustained conflict could be severe if investors lose confidence in the Gulf as an island of stability in a dangerous neighborhood. There is already speculation that a prolonged conflict could pressure Gulf economies and force reassessment of overseas investment commitments — a notable risk at a moment when Vision 2030 and similar initiatives depend on attracting, not repelling, global capital.

Iran’s Fragile Domestic Economy

Iran limped into the conflict with a fragile economy already weighed down by sanctions, high inflation, and currency volatility, and the war risks accelerating a shift toward an even more opaque, security-driven economic model dominated by the IRGC. Oil exports remain the regime’s primary economic lifeline, but a growing share of those barrels are now controlled by entities tied to the defense and security apparatus, which increasingly sell crude through sanctions evasion networks rather than formal markets.

Much of that system runs through the Gulf, particularly the UAE, which for years has served as one of Iran’s most important financial conduits for trade, payments, and front-company activity. Emirati officials are now reportedly exploring a far more aggressive step: freezing billions of dollars in Iranian assets and dismantling the shadow companies and currency-exchange networks that help Tehran access foreign currency and global trade. Analysts say such a move could significantly constrict Iran’s access to hard currency, because Dubai has functioned as the central hub for processing payments tied to Iranian oil sales and other sanctioned commerce.

If these channels tighten, Tehran is likely to rely even more heavily on alternative mechanisms that have expanded in recent years, including barter trade, a shadow fleet of aging tankers used to move sanctioned crude, and crypto-based financial networks used to route payments outside the formal banking system.

The result would not necessarily collapse Iran’s economy in the short term. The regime has shown creativity, and proven adept at operating in gray markets. But it would further entrench a wartime economic structure in which state security organs, sanctions evasion networks, and informal finance increasingly substitute for normal trade and investment, deepening the long-term structural weaknesses of Iran’s economy even as the regime preserves its immediate access to cash and perpetuating structural sources of suffering and grievance among many ordinary Iranians.

Spoiler Alert[s]

Even if the core military confrontation remains geographically contained, a wide range of spoilers could expand the conflict in unpredictable ways. Cyber activity is already rising sharply: security researchers and Google’s threat analysis teams have reported a surge in Iran-linked cyber operations targeting governments, infrastructure, and tech firms worldwide, suggesting Tehran may increasingly rely on digital disruption as a low-cost way to impose economic pain on adversaries without escalating kinetically. Beyond cyberspace, the greater risk could be asymmetric retaliation. Iran historically does not respond in strictly linear fashion. Instead, it has relied on deniable networks and proxy actors capable of striking soft targets abroad, particularly Western, Israeli, or Jewish-linked institutions, a pattern seen in past attacks from Buenos Aires to Burgas.

Meanwhile, external powers are beginning to appear at the margins of the conflict. Neither Russia nor China has provided overt military backing, but reports that Moscow may be sharing satellite imagery or targeting data with Tehran and that Chinese firms are allowing shipments of key rocket precursors to reach Iran during wartime point to a quieter form of support that could gradually alter the battlefield. Beijing’s posture is particularly notable: facilitating such shipments represents a more forward-leaning stance than China has historically taken in Middle Eastern armed conflicts and could risk friction with Gulf Arab states that are major suppliers of oil to China and important markets for Chinese exports.

Finally, internal fragmentation within Iran itself could create unintended consequences. Reports that Kurdish armed groups, some allegedly backed by Western actors, are expanding activity along Iran’s borders may weaken the state in the short term, but could also fracture the broader opposition landscape, potentially strengthening the IRGC’s narrative that the country faces foreign-backed destabilization. In other words, the longer the conflict continues, the greater the chance that actors operating at the periphery (e.g. cyber units, proxy networks, opportunistic great powers, and internal insurgent groups) could reshape the conflict in ways none of the principal combatants fully anticipate or control.

What to Watch Next

The Iran conflict’s economic consequences are already spreading well beyond the battlefield, but the ultimate trajectory will likely depend on three interrelated variables: duration, geographic spread, and market confidence. In the near term, the most visible shocks are in energy markets and global trade logistics, where disruptions to the Strait of Hormuz and regional infrastructure are pushing up oil prices, shipping costs, and insurance premiums while forcing companies to reroute supply chains across longer and more expensive routes.

But the deeper question is likely whether the conflict begins to erode the broader economic architecture the Gulf has spent the last decade building, one centered on stability, open trade corridors, and the region’s emergence as a safe destination for global capital. If hostilities stabilize relatively quickly and shipping flows resume, markets may ultimately treat the episode as another geopolitical risk premium layered onto Middle Eastern assets. If the war drags on, however, the consequences could extend much further: Gulf states may move toward tighter security alignment with Western partners, investor confidence in hubs such as Dubai or Riyadh could be tested, Iran’s economy may retreat further into sanctions evasion networks dominated by the IRGC, and spoilers could widen the conflict’s economic footprint.

In short, while the Middle East has historically absorbed volatility, the scale of this confrontation means the stakes are higher: what began as a military crisis is increasingly becoming a test of whether the region’s economic integration with global markets can withstand sustained geopolitical shock against the backdrop of behavior from the US and Israel that is anything but predictable.